Payroll Legislation Hub

The latest

payroll legislation

news & updates

Your database for all the latest updates to UK payroll legislation to keep you in the know, and most importantly, keep your payroll compliant.

Join Cintra's newsletter

Cintra HR & Payroll Services needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at any time. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, please review our Privacy Notice.

Payroll deductions

2026/27 Payroll Legislation Guide

The facts, figures, thresholds and allowances for 2026/27 spanning tax, National Insurance, pensions, statutory payments and more—in one handy guide.

Download your 2026/27 payroll legislation guide

Latest news

HMRC Payrolling Benefits: What Does the Phased Plan Mean?

Mileage Rate Increase 2026: What UK Employers Need to Do Now

Key Payroll Changes for 2026/27

Documents

Leave entitlements

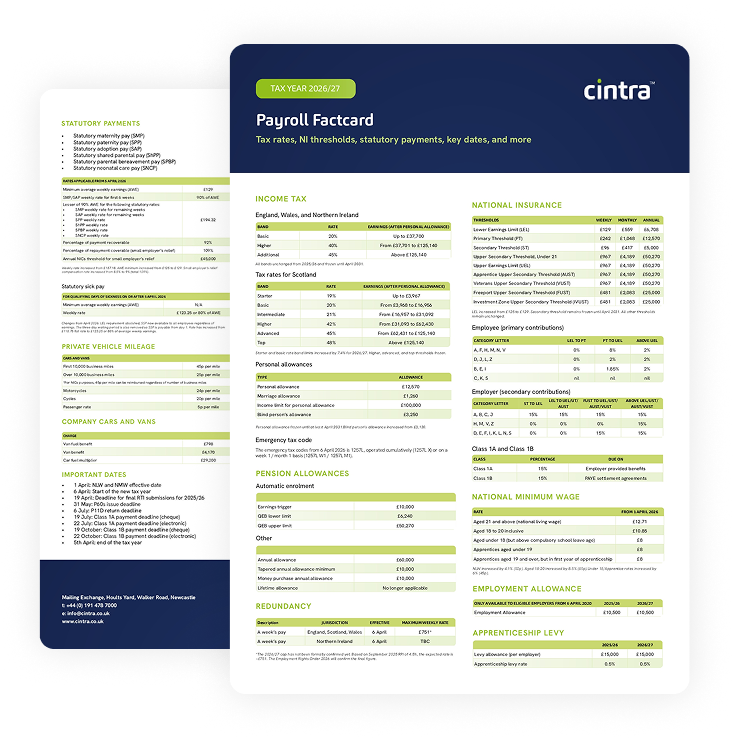

Payroll Factcard

Get all the facts and figures for the 2026/27 payroll year in one simple, straightforward document.

Download your payroll factcard

Looking for regular updates?

From monthly round-ups to actionable best practice… Sign up to receive updates directly in your inbox!

Sign up now

Cintra HR & Payroll Services needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at any time. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, please review our Privacy Notice.

Payroll glossary

We know that understanding the terminology that comes with payroll and legislation updates can be a little tricky, so we’ve created an A – Z of keywords to help you navigate our updates.

Apprenticeship levy

The apprenticeship levy is basically a tax paid by large employers, which goes into a fund available to help businesses pay for apprenticeship training costs. All employers with an annual pay bill of more the £3 million pay the levy at a rate of 0.5% of that bill

Attachments of earnings

When an employee is fined by a court, their employer can be required to make deductions from their wages towards the amount owed. The court will issue an ‘attachment of earnings order’ (AEO) to both parties, explaining how much the employee owes, how much is to be taken from their wages each pay day and the minimum amount they must still take home. The employer then sends the money deducted to the court

Automatic enrolment

Automatic enrolment simply means that eligible employees are included in a workplace scheme automatically, where the employer and employee make contributions into the pension. (They can then opt out, but will be re-enrolled again on the anniversary on their enrolment date). To be eligible, employees must be between 22 and State Pension age and earn a certain amount per year (subject to change).

BACS

BACS (formerly Bankers’ Automated Clearing Services) is the electronic system for bank transfers in the UK and is the standard body for the UK’s retail interbank payment systems. Most of us today have our salaries paid directly into our bank accounts and pay our own bills more or less the same way. BACS is just the digital technology behind all that. It’s owned and operated behind the scenes by a body called Pay.UK since 2018. Pay. UK provide the digital payments networks used by the UK’s banks, building societies, other payment providers and all their customers to make payments, making sure they are secure, safe and simple to use.

Benefits in kind

Benefits in kind are goods or services that are provided to an employee free or at a significant discount, effectively as a supplement to pay. However, that means they have to pay tax on them! Benefits in kind should not be confused with perks like free coffee and biscuits or gifts from an employer, which thankfully are not taxable. Employers are legally obliged to provide their employees with details of relevant benefits each tax year. A P11D form is then used to report benefits in kind to HMRC. Alternatively, the tax can be paid directly through payroll.

Chartered Institute of Payroll Professionals (CIPP)

The CIPP does what it says on the tin. It supports people who work in payroll by providing educational resources, training and professional accreditation, and it represents their views to government when it comes to relevant legislation. The institute also offers compliance ‘health checks’ to help organisations make sure they’re complying with current legislation.

Deductions

These are the sums of money which can be taken away from your payroll, for example tax, pensions and national insurance are al deductions.

Employee self-service (ESS)

ESS is essentially the term used for employees being able to ‘help themselves’ to information and services that would traditionally have been dealt with by HR departments. Many organisations now offer platforms like intranets or web portals that allow people to update their own contact information, enrol in benefits, download records of pay and even request time off.

Employment allowance

The employment allowance is meant to help smaller employers manage their employment costs. Simply put, it lets them reduce the amount of National Insurance they pay. To qualify, they must be a business or charity with employers’ Class 1 National Insurance liabilities below the thresholds set out by HMRC. Businesses that employ a care =or support worker can also claim the allowance.

Employment income manual

This manual is a resource produced by HMRC to explain in plain English what the law requires of employers in terms of payroll. In particular, it covers the Income Tax (Earnings and Pensions) Act 2003 and provides details on ‘Employment income’, ‘Termination payments and benefits’ and ‘Deductions from general earnings’. Nobody’s idea of a gripping read, it does at least help keep employers on the right side of the law.

Employment status manual

This manual from HMRC tells employers everything they need to know, in more or less straightforward language, about the legal status of their employees. For example, it unpicks the sometimes-knotty question of whether someone is technically employed or self-employed. (This is no doubt a well-thumbed volume at Uber.) It also deals with the complexities that arise when it comes to agency and temporary workers.

Employer payment summary (EPS)

EPS is a report sent in real time to HMRC using payroll software. You’ll only really need an EPS if no employees were paid in the tax month, but best practice is to send it. There are detailed government guidelines available in case of doubt. Otherwise, payroll reporting is all about the FPS.

Expenses

When employees spend their own money in the course of their work, these expenses can be claimed back from the employer. Expenses can be paid on a one-off basis or incorporated into payroll, so employees are reimbursed when their salary is paid. Expenses can include everything from working materials to food and entertainment, as long as they’ve been agreed by their managers. And they’re based on a vouched receipt, so don’t forget to keep them on hand!

Full payments submission (FPS)

Employers are required to keep HMRC updated on their payroll and employees’ tax and National Insurance. An FPS is a report sent as Real Time Information every time employees are paid. As well as statutory payments and deductions, it includes other information about employees’ pay, such as; payrolled benefits, updates on any starters or leavers and links with DWP (Department for Work and Pensions) for the assessment of benefits. An FPS is sent using payroll software, which makes it a lot easier that it would otherwise be.

Full-time equivalent (FTE)

With more people today working part-time or irregular hours, it can be hard for employers to get a sense of who is doing what and how long various tasks actually take. FTE is a standardised method of measurement that allows them to compare the cost and effectiveness of all employees by dividing the actual weekly hours worked by the hours in a full working week, typically 40. That way, they know if they’re getting bang for their buck.

General Data Protection Regulation (GDPR)

Originally an EU regulation but now incorporated into UK law, the GDPR is meant to protect people’s personal data. All companies are required to be GDPR compliant, which means things like consolidating personnel and payroll data into as few locations as possible, and making sure everything from sick notes to timesheets are kept away from prying eyes. It’s important to get this right, as there are severe penalties for violations.

Gender Pay Gap

The gender pay gap is the difference between average earnings of women and men. While it has been illegal since the Equal Pay Act of 1970 to pay men and women differently for the same work, the gap persists for a variety of reasons. From an employer’s perspective, it’s important that one of those reasons is not you. All organisations with over 250 employees are legally required to identify and publish details of their gender pay gap, so there’s no hiding it!

HMRC

HM Revenue and Customs is a department of the UK Government responsible for the collection of taxes, providing national insurance numbers, and the administration of other regulatory rates including the national minimum wage.

IR35

The origins of the term IR35 are lost in the mists of time, but basically it refers to off-payroll working rules. These apply if someone provides services through their own limited company or another intermediary and are meant to make sure they pay broadly the same Income Tax and National Insurance contributions as employees. Since 2021, it has been the responsibility of employers—not employees—to determine when these rules apply, and if necessary to add the ‘supplier’ to the payroll.

National Insurance

National Insurance contributions (NICs) go towards state benefits like the NHS, unemployment benefits, and the State Pension, and in many cases, employees need to have paid National Insurance to qualify for these benefits. Employers deduct contributions from pay just as they do with Income Tax, as well as making their own contributions for each employee. The amounts vary depending on the employee’s particular National Insurance category tax status. Each employee’s unique National Insurance number also serves as a useful form of identification, allowing contributions to be allocated to the employees account.

National living wage

There comes a point in life when someone comes to need and expect a higher standard of living than they might settle for as a student or an office junior living at home. According to the government, that point is at age 23, when they qualify for the national living wage rather than the minimum wage—see below. Like the minimum wage, the living wage goes up periodically to keep up with the cost of living. Employers who fail to keep up face legal sanctions. Plus, any salary sacrifice schemes in operation have to be taken into consideration when calculating national living wage

National minimum wage

Since 1998, all UK employers have been obliged to pay people no less than a set amount known as the national minimum wage. Believe it or not, this was originally as little as £3.00 an hour, so for obvious reasons it has risen periodically ever since, typically going up each year with the government’s Spring Budget. There are different rates for those under 18, from 18 to 20 and from 21 to 22. From 23, employees get the national living wage—see above. Like national living wage, employers need to bear in mind their salary sacrifice schemes when calculating national minimum wage.

Outsourcing (also known as fully managed service)

Would you rather not be reading this glossary? If so, you will see the appeal of outsourcing the payroll function completely. A fully-managed payroll service is one provided by a third party that manages the gross to net payment function and supports you with UK payroll legislative requirements.

P2

This is the first of many Ps, which take their names from numbered forms in the Dark Ages of paper tax filing. Also known as a notice of coding, a P2 form is issued directly to employees by HMRC at the start of each tax year and states an employee’s current tax code. Helpfully, it also explains why it is what it is. It will mention any relevant job expenses or company benefits and for example, if the employee has underpaid tax in a previous year.

P6

This form was used by HMRC to inform employers of a change to an employee’s tax code, so that’s what P6 means today, even though it comes as an email alert via the HMRC gateway. The new code is to be used from the next pay day onwards.

P9D

The P9D has now passed on, is no more, has ceased to be. It was formerly used to report details of expenses and benefits for each employee earning less than a certain amount in a tax year. That information is now added to the very much alive P11D.

P11

Another expired P, the P11 or Deductions Working Sheet was once used to record information about payments and deductions made to employees’ pay. Since the glorious advent of Real Time Information (RTI), this information has been included in the relevant fields within the Full Payment Submission (FPS) or Employer Payment Summary (EPS).

P11D

A P11D is one of the ways of reporting on benefits. Employers use the P11D, or expenses and benefits form, to submit an annual report to HMRC for each employee or director who has received expenses or benefit in kind, like company cars, private health insurance or childcare, or travel costs. While we’re here, the P11D(b) is used to report the Class 1A National Insurance contributions (NICs) due on such expenses and benefits.

On the other hand, a Nil P11D is a declaration of no return of Class 1A National Insurance Contribution. If you’ve submitted a P11D in the past but have none this year, you’ll have to let HMRC know by submitting a Nil P11D. Without this, HMRC will be expecting you to submit a P11D, and you could be charged a penalty for non-submission. This only needs to be completed in the first year where no benefits were provided, instead of having to be ubmitted each year.

P14

Yet another expired P, the P14 used to be completed at year end for each employee who earned the Lower Earning Limit or above. The relevant information is now included in the Full Payment Submission (FPS) or Employer Payment Summary (EPS).

P45

When someone leaves their employment, whether fired, quits or leaves by mutual consent, their former employer must provide them with a P45. It shows how much tax they have paid in the current tax year, as well as including their address and National Insurance number.

This makes it easy for their new employer to set them up on their own payroll system. A duplicate cannot be produced, so a starter checklist should be completed instead.

P46

The last of the obsolete Ps, the P46 was once completed by employees who did not have a P45, e.g., because they were continuing with their previous job as well as starting a new one. The ‘starter checklist’ now provides the details needed.

P46(Car)

A P46(Car) form is something still used when a company car is provided or withdrawn from an employee, but this can also be done electronically.

P60

Without doubt every payroll professional’s favourite P, the P60 shows how much tax an employee has paid during each tax year. At payroll year end (see below), employers must give each employee a P60, either on paper or electronically. The latest it can be provided is 31 May, so the employee has time to check it before filing any tax return. Employees can use their P60s to prove how much tax they’ve paid and make any claims. They also serve as proof of income when applying for a loan or a mortgage.

This applies to anyone on payroll at the end of the tax year (5th April). For employees that left on or before that date, it will be down to their new employer to provide them with a P60.

PAYE

PAYE stands for Pay As You Earn, and refers to the way employers deduct tax and National Insurance contributions directly from earnings and pay it to HMRC on employees’ behalf. This is typically done by BACS, and details must be sent by RTI (see below) via payroll software. This means employees pay their tax without having to do anything or even think about it.

PAYE manual

The whole point of PAYE is that it’s automated, so this has nothing to do with doing things manually. The PAYE manual is a guide produced by HMRC to help employers understand how the PAYE system works, everything they need to know about RTI and more. It also has a glossary of terms, but it’s considerably less entertaining than this one!

PAYE online

Straightforwardly enough, PAYE Online is HMRC’s online service for payroll. Employers are required to register, and can then input their PAYE Online account details into their payroll software to use Real Time Information (RTI). Crucially, this means PAYE Online is not a substitute for payroll software, which is still needed to send electronic payroll reports to HMRC. It can however be used on its very own desktop viewer as well as on a web browser – if downloading yet more software is your thing.

Payment after leaving (PAL)

Once an employee has left a company, it sometimes turns out they are owed money for unpaid wages or for some other reason. If their employment has already been terminated and a P45 produced, however, they obviously cannot be paid through normal payroll. So a PAL is a special payment processed separately, and a real ‘pal’ to the bank balance. The employee will not receive another P45 but HMRC will be informed of the payment.

Payrolled benefits

Payrolling benefits is a way of paying tax on benefits in kind (see above) on a month by month basis. If that sounds like common sense, it is, but it used to be that employers had to fill out all of the information on a P11D at the end of each tax year, and their employees paid the tax in the following year. They can still do it that way if they prefer!

Payroll year end

The highlight of the HR year is the ancient festival of ‘Tax year end’, officially observed on 5 April. Payroll professionals celebrate by submitting their final payroll reports to HMRC and updating employee payroll records in preparation for the new tax year starting on 6 April. Employees are given gifts in the form of a P60 (see above). Festivities then spill over into the following months, as the previous year’s expenses and benefits (like P11D’s) must be reported to HMRC before 6 July, and Class 1A National Insurance is due on taxable expenses and benefits by 22 July.

Personal allowance

This is the amount of money employees are allowed to earn each tax year before they start paying Income Tax, and also defines an employee’s tax code. It’s subject to change year on year, depending on how generous the government of the day is feeling. Employees who earn less than the personal allowance usually don’t have to pay any Income Tax (which is just as well, as the amount is never huge). The relevant figure might be higher for employees who claim Marriage Allowance or Blind Person’s Allowance. High earners have a lower allowance.

Real Time Information (RTI)

In the olden days, employers would wait till the end of each tax year before sending HMRC details of who was paid what for tax purposes. This involved lots and lots of paper. Nowadays, the same information is sent online ‘in real time’ using payroll software. That means HMRC are informed whenever employees are paid, whether that’s weekly, monthly or quarterly. Usually, all that’s needed is a Full Payment Submission (FPS), but sometimes it will have to be supplemented by an Employer Payment Summary (EPS).

Redundancy payment thresholds

When an employee is made redundant, their employer is usually obliged to make a payment to compensate them for loss of earnings. This amount is based on what they were paid and how long they worked for the employer, but only up to a point. So, their payment calculation is based on maximum weekly amount, even if they were paid more, and is capped at a maximum total amount. Both are subject to change.

Salary journal

Nothing to do with ‘Dear Diary’, a salary journal is a comprehensive record of a company’s payroll information. For each employee, it will include gross pay, net pay, Income Tax deductions, National Insurance Contributions and pensions and other deductions. This is typically incorporated into payroll software and is particularly useful for accounts to allocate costs.

Salary sacrifice

Not nearly as scary as it sounds, a so-called salary sacrifice arrangement simply means part of an employee’s cash salary is replaced with something else, usually a non-cash benefit. The employee must agree to this substitution, which means they believe the alternative benefit is worth having, and it must be set out in their employment contract. Importantly, their cash earnings must still be in line with the national minimum wage.

Shared parental leave (SPL)

Not nearly as scary as it sounds, a so-called salary sacrifice arrangement simply means part of an employee’s cash salary is replaced with something else, usually a non-cash benefit. The employee must agree to this substitution, which means they believe the alternative benefit is worth having, and it must be set out in their employment contract. Importantly, their cash earnings must still be in line with the national minimum wage.

Small employers' relief

Small employers’ relief is there to help smaller businesses manage their costs. Like other employers, those with small businesses can claim money back from the government to cover the cost of paying statutory parental payments. A small company—one whose total employer and employee liability for national insurance contributions is under the HMRC threshold—can reclaim 100% of that money, plus 3% for good measure.

Starter checklist

The starter checklist is a document produced by HMRC to help employers gather essential information about new employees in the absence of a P45 (see above). It includes questions about their general personal details and circumstances, including whether they’ve been claiming benefits or have student loans. The idea is to make sure they don’t pay too much or too little tax. Employers have to keep this information for the current and next three tax

years.

Statutory Adoption Pay (SAP)

Employees who adopt a child or have a baby through surrogacy are entitled to a payment from their employer that helps them take time off work to look after the child. Frequency of the payment depends on the employers payroll frequency and only one parent can claim SAP.

Statutory Maternity Leave

New mothers are legally entitled to take up time off without compromising their right to pay rises, holiday accrual etc. Statutory Maternity Leave comprises 26 weeks of ‘ordinary maternity leave’ and 26 of ‘additional maternity leave’. All are optional except for the first two weeks, or four if they work in a factory. Leave can start as early as 11 weeks before the baby is expected, but the mum-to-be must tell her employer at least 15 weeks before that date. She is also allowed to work up to ten keeping-in-touch (KIT) days, if agreed with her employer, without losing any of the rights afforded by Statutory Maternity Leave.

Statutory Maternity Pay (SMP)

Babies being notoriously expensive, new mothers who are eligible for Statutory Maternity Leave might also be able to claim Statutory Maternity Pay for up to 39 weeks during the leave. And they’ll have to pay tax and National Insurance on that money. Amounts are subject to change, but a Statutory Maternity Pay calculator can be found at gov.uk. Note that different rules can apply to agency and educational workers and directors.

Statutory Paternity Pay (SPP)

Like Statutory Maternity Pay, but for Dad. But only lasts 2 weeks maximum and must be taken all at once.

Statutory Paternity Bereavement Pay (SPBP)

We hope very few people will ever need this one. It provides parents who lose a child or suffer a stillbirth with the right to take two weeks off work with statutory pay.

Statutory shared Parental Pay (ShPP)

As with Shared Parental Leave (SPL), both new parents might be able to claim Statutory Shared Parental Pay (ShPP) for the period of leave. They can claim up to 90% of their average weekly earnings for that period, or an amount set by the government if that is lower.

Statutory Sick Pay (SSP)

SSP kicks in as soon as an illness keeps someone from work—the previous three ‘waiting days’ have been abolished, meaning SSP is now payable from the first full day of sickness absence. Employees are entitled to £123.25 per week or 80% of their normal weekly earnings, whichever is lower, and can claim for up to 28 weeks. Tax and National Insurance are still deducted. After seven days, the employer can ask for a note from a health professional to confirm the person is unable to work. To qualify, the claimant must be an employee rather than a worker and must have started the job. The Lower Earnings Limit has been removed, meaning SSP is now available to all eligible employees regardless of their earnings.

Student loan

Many people look back on their student days as the best time of their lives. How fortunate, then, that they have loan repayments to remind them of those happy days for years afterwards. But unlike conventional loans, student loans do come with some wiggle room. Graduates only have to make repayments if and when they begin earning a certain amount, and repayments are then made directly by their employer—although it’s the employee’s responsibility to liaise with the Student Loans Company. That threshold varies depending on the repayment plan in question.

- Plan 1 applies to English or Welsh students who started undergraduate courses

before 2012, and Northern Irish students after 1998. - Plan 2 applies to Welsh students who started after 2012 and English students

between 2012 and 2023. - Plan 3 is now just called the Postgraduate Loan Plan, because that’s what it’s for.

- Plan 4 applies to Scottish students.

- Plan 5 applies to English students starting after 1 August 2023.

Tax code

Tax codes are a series of letters and numbers that tell employers how each individual employee should be taxed. They indicate how much personal allowance they have in any given tax year and how tax should be deducted from the rest of what they earn. A new employee’s P45 is used to determine their tax code—typically using payroll software—and if their circumstances change and that code needs to be updated, HMRC will notify their employer. A full list of tax codes and their meanings can be found at gov.uk.

Worker

In employment law, ‘workers’ can undertake casual or irregular employment without the kind of written contract that makes someone an ‘employee’. And

while both have basic rights like receiving the minimum wage and paid holiday, workers have fewer rights in terms of protection against unfair dismissal, statutory redundancy pay, the right to request flexible working and so on.

Statutory rates archive

See Cintra in action

We’ll show you Cintra’s cloud-based software, and you tell us about your needs and challenges. Together, we’ll find the perfect payroll and HR solution for your organisation that keeps you fully compliant.

Ready to see a Cintra demo?

Share your contact details with us and we’ll be in touch soon.